Thomaz Monteiro

The Catalyst Group’s Thomaz Monteiro, Director – Compliance, Legal & Governance, discusses the rationale behind having an offshore fund – from a Brazilian perspective, and the key considerations from a KYC/AML, operations, and costs perspective.

Typically, the decision to establish a fund in Cayman, or any other jurisdiction (BVI, Bahamas) by a Brazilian investment manager, will be driven by two key factors:

The investment manager’s desire to invest into assets and products that are either only accessible once you establish an offshore structure or that the direct investment from Brazil is not tax/cost efficient; and the capability of raising international capital to flow into Brazil or, in some cases, to make investments in other regions, especially within the US, with no direct ties to Brazil.

In this article, The Catalyst Group’s Thomaz Monteiro, will be focusing on the first of the two scenarios described above.

Brazilian Funds as investors – key aspects of investing into an offshore fund

From the perspective of its financial and capital markets, Brazil is still a jurisdiction with relatively limited internationalisation. However, in recent years, the process of market integration, the strengthening of business environments and the growth of participants with international reach and presence, has made this issue more relevant and prevalent in the national dialogue.

Agendas for flexibility and modernisation in the foreign exchange market, regional integration for business and infrastructure, and simplification of regulations applicable to non-residents represent some of the topics that have been frequently discussed.

Many of these issues have been partially addressed by the new Resolution CVM 175/22 (Resolution 175), the new regulatory framework for investments funds in Brazil. This was due to come into force this month but has now been delayed until October of this year.

KYC/AML

It is worth noting that historically, the role of the fund administrator in Brazil has been very different when compared to that of offshore administrators.

The differences were intrinsically linked to the fact that Brazilian funds are organised as condominiums, without legal personality, which, is very different to offshore funds, which are typically organised as companies or limited partnerships.

This means that Brazilian funds do not have principals such as a director or a general partner.

Before Resolution 175, the administrator was much more than a simple service provider. Instead, they were the ones responsible for almost all the obligations imposed by the local regulation. This included that the creation of the fund was, as per Brazilian rules, a decision made by the administrator, who would then hire the investment manager, who in turn would be responsible for taking care of the investments of the fund.

The intention of the regulator was to concentrate the power and the responsibility of creating investment funds among a few solid players, mostly well-established banks.

The aim was to allow for more effective supervision and, at the same time, ensuring that all stakeholders, especially the investors, would have some sort of recourse in a country that not long ago was still battling against astronomical inflation rates and political instability.

However, the Brazilian capital market has experienced a significant increase over the past 10 years and there has been increasing demand to make the industry more flexible and more closely aligned with international standards.

With the implementation of Resolution 175, investments funds will be jointly created by all the main service providers, including the IM and the administrator, whose duties and responsibilities are now better segregated.

Besides other things, Brazilian funds will now be allowed to have different classes, and investors will be able to have limited liability as opposed to the unlimited liability under the previous regulation.

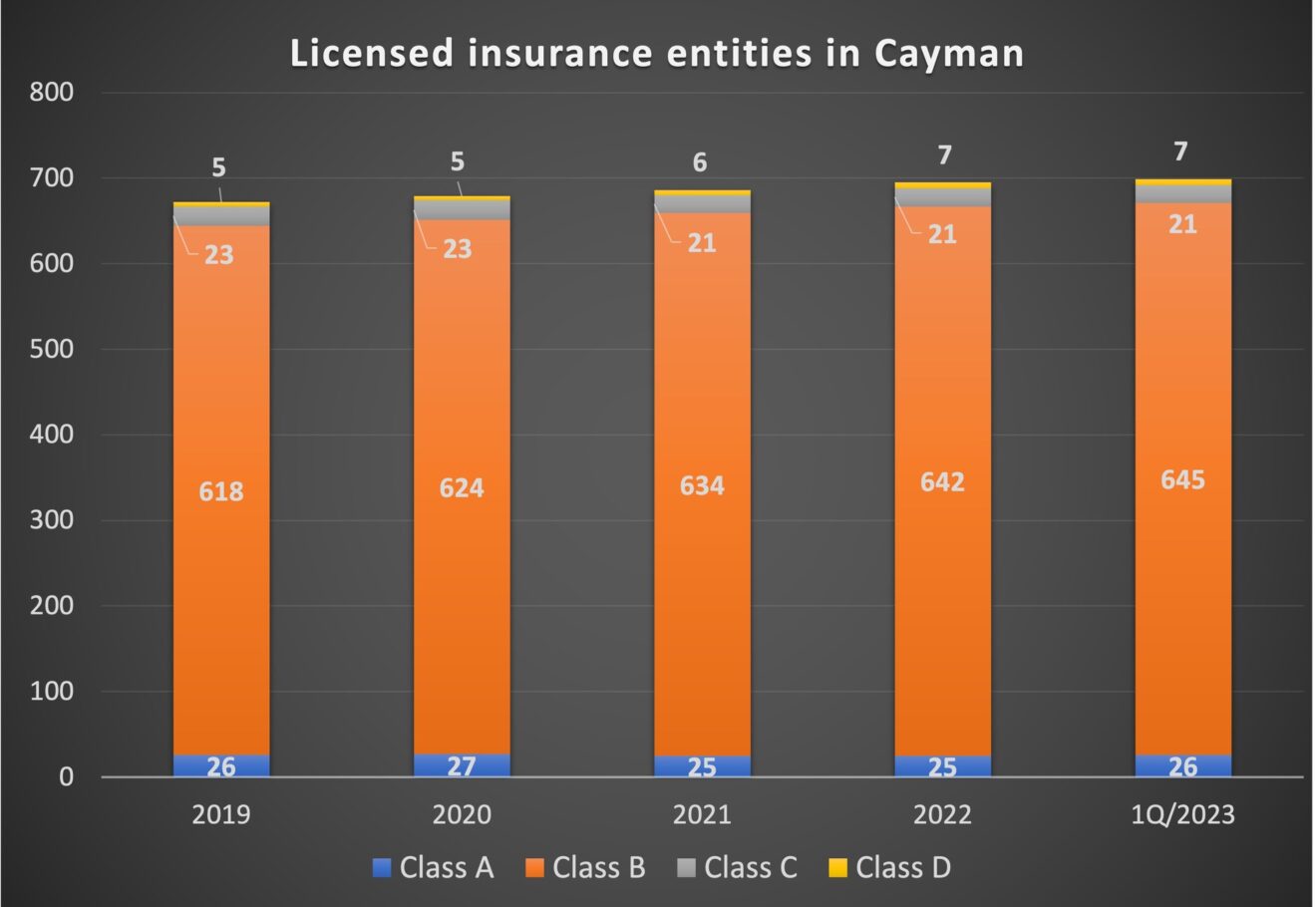

These changes have been introduced to help modernise the industry but at the same time keep Brazilian funds subject to the very strict regulations established by the Comissão de Valores Mobiliários (CVM), the Brazilian equivalent of the Securities and Exchange Commission in the US, and the Cayman Islands Monetary Authority (CIMA) in Cayman.

The CVM is recognised worldwide for having high standards of regulation and transparency requirements from its regulated participants, and just as an example, has had a Memorandum of Understanding in place with its Caymanian counterpart CIMA since 1999.

From an AML/KYC perspective, all investors that invest in a Brazilian fund are subject to an extensive AML/KYC and due diligence process, carried out by the administrator itself, the investment manager and/or distributor of the fund’s shares. These AML/KYC requirements come from federal laws, CVM regulations, and are in line with international standards.

It is for this reason that we are able to efficiently onboard a Brazilian fund as an investor of an offshore fund, irrespective of whether it is located in Cayman, BVI or Bahamas.

The comprehensive AML/KYC process simplifies much of the groundwork associated with the onboarding process of such an investor and facilitates subscription and redemption requests. This is one of the benefits that managers located in Brazil take into consideration when opening this type of structure.

Operations and costs

From an operational perspective, it is interesting to note that most Brazilian funds allow investors to subscribe and redeem on a daily basis, leading to the need for a valuation of the shares to be produced every business day.

This means when a Brazilian Fund invests into an offshore Fund, Brazilian managers would typically require this structure to also have the same flexibility. This in turn necessitate the delivery of a daily NAV by the administrator/NAV calculator of the offshore fund.

After the offshore fund is incorporated and all the documents are duly registered with the local regulator, the next step is to open a bank account (the RTA account) which will be controlled by the administrator/registrar and transfer agent (RTA).

This account is where the subscription funds sent by the Brazilian fund to acquire the shares of the offshore fund will be initially transferred.

Once the money arrives in the RTA account, the manager will then instruct the administrator/RTA to wire the money to a broker account where the investment trades will take place. All redemptions must also pass to that same cash account before being sent back to the investor in Brazil.

Finally, in terms of costs, all the formation expenses are typically born by the offshore fund itself and the respective provisions in the NAV can be made over an extended period of time (i.e., 12-months) so as to not have a significant impact on the first few months of the fund’s operation.

Thomaz Monteiro, is a Director – Compliance, Legal & Governance, at The Catalyst Group.