Japan’s investment landscape is undergoing significant transformation, with a growing interest among Japanese investors in private markets. Japan’s evolving economic conditions, coupled with demographic shifts, such as an aging population, are prompting Japanese investors to seek higher returns through alternative asset classes. This shift is creating a golden era for global asset managers, who are increasingly focusing on Japan’s investor-driven market evolution.

Institutional investors and market dynamics

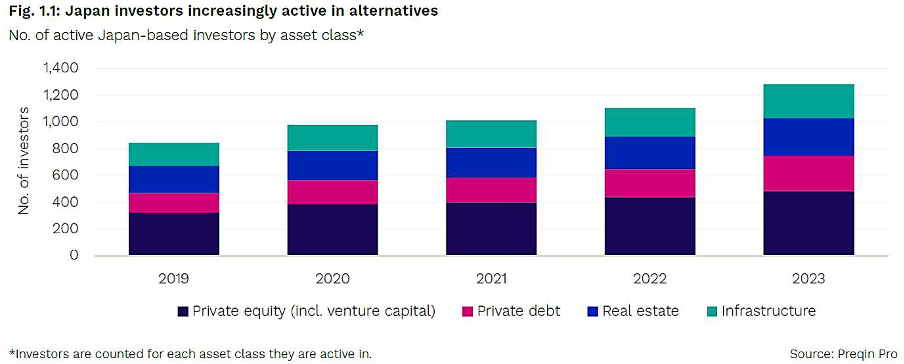

The growing interest in private markets among Japanese institutional investors has been providing substantial opportunities for global asset managers. The diversity of Japanese institutional investors and asset classes has expanded in recent years, drawing increased attention from international managers.

Japan’s rapidly aging population is likely to further drive institutional investors, such as pension funds and life insurers, toward alternative investments as they seek higher yields to meet increasing liabilities. Currently, 29.1% of Japan’s population is aged 65 or older, a figure projected to exceed 34.8% by 2040[1].

However, as of June 2023, Japan-based private capital funds manage assets totalling US$115 billion, according to Preqin data. This figure includes foreign investments but represents only about 4% of Japan’s pension fund assets. This proportion is insufficient to satisfy the investment needs of all Japan-based institutional investors, prompting them to allocate funds to international managers in the US, the EU and beyond.

HNWs, retail investors and government initiatives

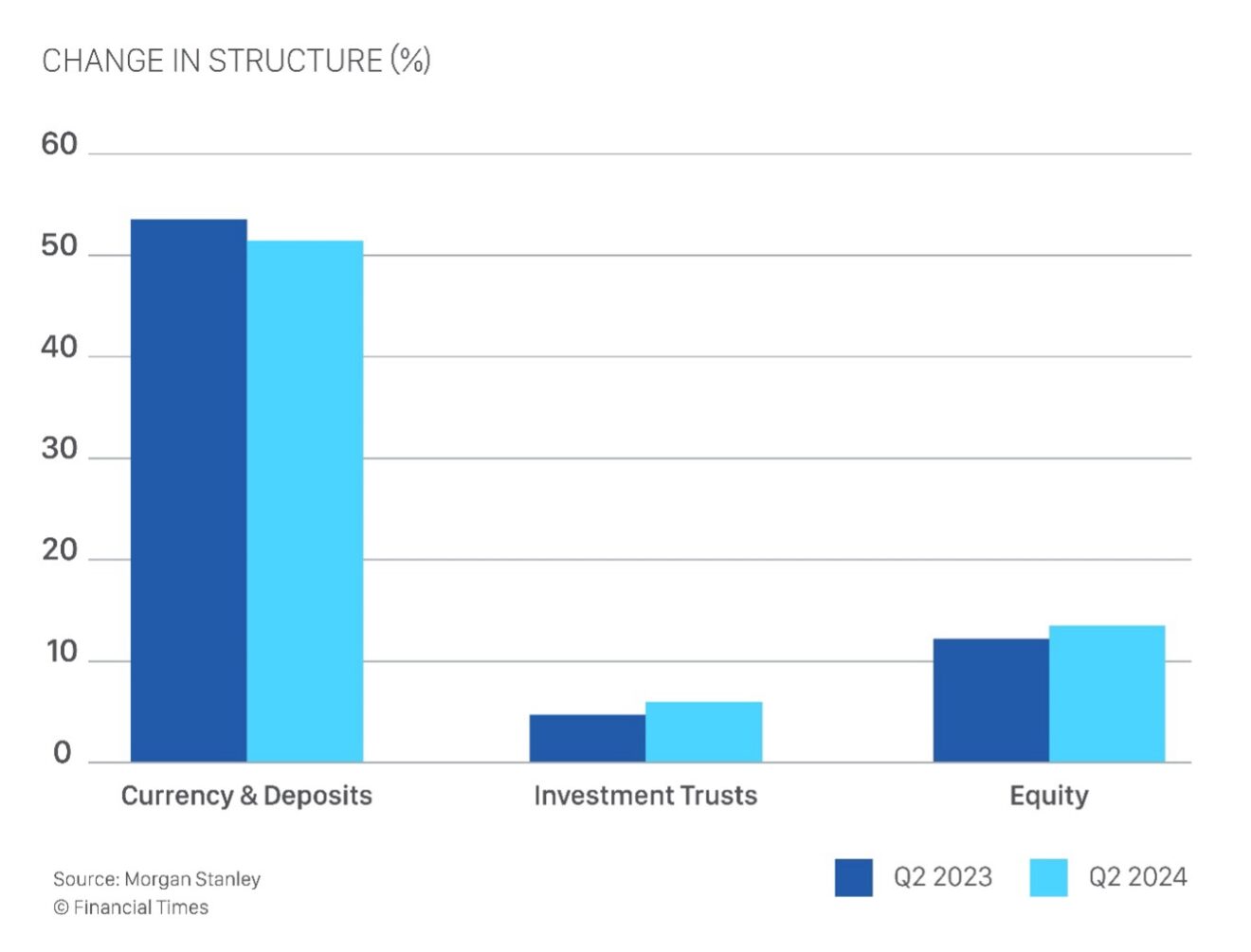

Japanese households possess approximately US$14 trillion in assets, with more than 50% of this amount held in cash and deposits[2]. In contrast, US households keep a mere 13% in similar liquid forms[3]. The Japanese government, acutely aware of the increasing pressures on the public pension system, is seeking to shift the national mindset from saving to investing and has a stated aim to double household investment income. One of the ways it is actively promoting investment is through the expansion of the Nippon Individual Savings Account (NISA), a tax-exempt investment scheme for individuals. The recent authorisation for investment trusts to include unlisted shares in NISA portfolios is anticipated to enhance retail access to alternative assets.

The result of these government initiatives has been an increasing number of private placement and public offerings of global asset managers’ semi-liquid funds in Japan, providing HNW and retail investors with exposure to private markets. It appears that these policies are beginning to have some success – the graphic below illustrates the beginning of the shift from cash to equities, although clearly there is still some way to go and, as a result, there remains significant opportunities for global asset managers.

Favoured asset classes

Private credit: This asset class is becoming more attractive to Japanese investors due to its potential for higher yields compared to traditional fixed-income products. The divergence in monetary policy between the Bank of Japan and other central banks has led to a devaluation of the Japanese Yen, making hedging against foreign bond investments more costly. As a result, investors are turning to private credit for its higher return potential.

Private equity: Japanese institutional investors are increasingly drawn to private equity for its potential to outperform traditional equity markets, and retail investors are following suit. The public offering in Japan of unit trusts that serve as feeders to private equity strategies is a notable example of this trend.

Real estate: Real estate is increasingly becoming a popular asset class among Japanese investors, driven by several compelling factors. The search for stable and predictable returns in a low-interest-rate environment has led investors to consider real estate as a viable alternative to traditional investment channels. The asset class offers the potential for capital appreciation and income generation, which is particularly appealing in the context of Japan’s aging population and the need for higher returns to secure retirement.

Infrastructure: With their stable, predictable cash flows often linked to inflation, infrastructure investments are increasingly favoured by Japanese institutional investors as a hedge against market volatility. Recent developments include the use of various fund structures to provide exposure to infrastructure investments.

Types of investment vehicles used by Japanese investors

Japanese investors utilise a diverse array of investment vehicles across various jurisdictions. The unit trust and the exempted limited partnership (ELP) are typically the investment structures of choice for Japanese investors. The ELP is particularly well-suited for situations where contractual flexibility and tax transparency are paramount. However, the surge in interest in alternative investments has also led to the development of a novel unit trust investment vehicle, the Private Equity Type Unit Trust. This structure can offer several benefits for investors seeking exposure to alternative investments, including investor familiarity, tax advantages, off-balance sheet accounting, and the potential for JPY hedging.

Conclusion

The increasing interest in private markets across all Japanese investor types, HNWs, retail and institutional, coupled with supportive government initiatives, presents significant opportunities for asset managers and is resulting in an increasing number of global asset managers entering the Japan market. Asset managers looking to capitalise on these opportunities should consider the unique preferences and needs of Japanese investors when structuring their investment products.

This article was first published in the AIMA Journal – Edition 141.

[1] National Institute of Population and Social Security Research

[2] https://asia.nikkei.com/Economy/Japan-households-financial-assets-hit-record-14tn-onstock-rally

[3] Financial Times article dated 14 December 2023 “Can Japan’s Legendary Savers Spark a Stock Market Boom”.

Nick Harrold is a partner in the Singapore Funds & Investment Management team at Maples and Calder, the Maples Group’s law firm.